Why Estate Taxes Hit Harder Than You Think — And What I Learned the Hard Way

I used to think estate taxes were just a “rich person problem” — until I saw how quietly they eroded my family’s wealth. It wasn’t about flashy assets or million-dollar homes; it was the overlooked details that cost us. Inheritance isn’t just about who gets what — it’s about what survives the transfer. This is how I uncovered the hidden risks no one talks about, and why planning ahead changed everything. The moment we realized a portion of my aunt’s estate would vanish before it reached her children, not to creditors or poor decisions, but to federal and state tax obligations, everything shifted. What felt like a distant concern became painfully real. We had assumed she wasn’t wealthy enough to be affected. We were wrong. And that mistake cost the family dearly in both financial loss and emotional strain.

The Wake-Up Call: When Inheritance Becomes a Financial Shock

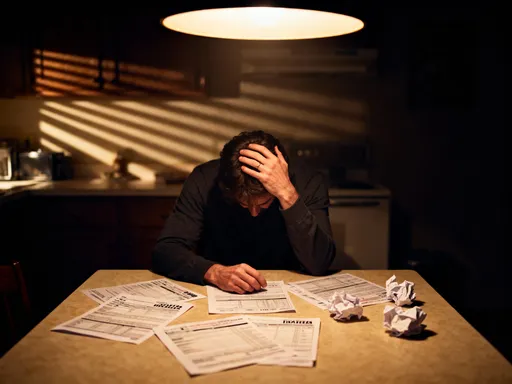

The first time many families confront estate taxes is not in a financial planner’s office, but in the quiet aftermath of a loved one’s passing. For my extended family, that moment came after my aunt passed away. She had lived modestly, owned a home worth about $900,000, and had modest retirement savings. No yachts, no second homes, no trusts we knew of. She had a will, named her two children as beneficiaries, and assumed that was enough. What none of us realized was that the combined value of her home, retirement accounts, life insurance payout, and personal investments pushed her estate just over the federal exemption threshold in that tax year. The result? Over $120,000 in federal estate taxes, plus an additional $45,000 in state inheritance taxes. That meant nearly 20% of her estate disappeared before any heir saw a dollar. The shock wasn’t just the number — it was the irreversible nature of it. This wasn’t a debt she had accumulated; it was a tax levied on the transfer of what she had built.

Estate tax, at its core, is a federal tax on the transfer of a person’s assets after death. As of recent tax law frameworks, the federal government allows a certain amount — known as the exemption threshold — to pass tax-free. In recent years, that figure has hovered around $12 million for an individual, but it is subject to change based on legislation. Many people assume this means only the ultra-wealthy are affected. However, state-level inheritance or estate taxes often have much lower thresholds. Some states begin taxing estates valued at $1 million or less. This is where the danger lies: families who consider themselves middle-class can unknowingly fall into taxable territory when real estate values rise, retirement accounts grow, or life insurance policies pay out. The tax doesn’t care about your self-perception of wealth — it cares about the total value of what’s being transferred.

The emotional toll of this realization is profound. One of the children had planned to keep the family home, a place filled with memories, as a legacy for the next generation. But without sufficient liquid assets to cover the tax bill, they were forced to sell. What was meant to be a gift became a financial burden. Family meetings turned tense, not because of greed, but because of confusion and unpreparedness. This is the true cost of estate taxes: they don’t just reduce the amount of money passed down — they disrupt the emotional continuity of a family’s story. The lesson was clear — estate planning is not a luxury for the rich. It is a necessity for anyone who wants their hard-earned assets to actually reach the people they love, in the way they intended.

The Hidden Traps: Common Misconceptions That Create Risk

One of the most dangerous aspects of estate planning is the confidence people place in incomplete or outdated strategies. Many believe they’ve done enough simply because they’ve taken a basic step — writing a will, naming a beneficiary, or buying life insurance. But these actions, while important, often fall short of addressing the real risks. The first myth I encountered was the idea that life insurance solves everything. My aunt had a $500,000 policy, which she believed would “cover any costs” and leave something extra for her children. What she didn’t know was that the death benefit, if paid directly to the estate or even to a beneficiary, could be included in the total estate value for tax purposes. In her case, that single policy pushed her estate over the state’s taxable threshold, triggering an additional tax liability she never anticipated. Life insurance is a powerful tool, but when structured incorrectly, it can become a tax accelerator rather than a safety net.

Another common misconception is that joint ownership automatically avoids estate taxes. Many parents add a child’s name to their home deed or bank accounts to “simplify things later.” While this may avoid probate in some cases, it does not eliminate tax exposure. The IRS still considers the full value of jointly held assets part of the deceased’s estate if they were the primary contributor. In one instance, a family friend believed that placing his vacation cabin in joint tenancy with his son meant it would pass tax-free. However, because he had paid for the entire property, the IRS included its full market value in his estate. Worse, the transfer created capital gains complications for the son when he later sold it. Joint ownership can also lead to unintended consequences during life — such as creditor claims against the co-owner or loss of control over one’s own assets.

Then there’s the belief that a will is enough. This is perhaps the most widespread and damaging assumption. A will is essential for naming beneficiaries and guardians, but it does not reduce estate taxes, avoid probate, or provide liquidity. In fact, probate can be a lengthy and public process, during which assets are frozen and taxes must still be paid on schedule. A will tells the court who should get what, but it doesn’t tell the IRS how to treat the estate. Without additional tools like trusts or gifting strategies, even a well-drafted will leaves families vulnerable. I’ve come to see these misconceptions as traps not because they are malicious, but because they offer a false sense of security. They are like wearing a raincoat during a hurricane — technically prepared, but fundamentally unprepared for the scale of the storm. True protection comes not from isolated actions, but from a coordinated, forward-looking strategy.

Asset Mapping: Seeing Your Estate the Way the IRS Does

After my aunt’s experience, I decided to take a hard look at my own financial picture — not just what I owned, but how it would be seen by tax authorities. I sat down with a financial advisor and began what I now call an “estate audit.” This wasn’t about net worth for bragging rights; it was about clarity. The first step was listing every asset, no matter how small. Real estate, bank accounts, retirement funds, life insurance policies, brokerage accounts, business interests, and even digital assets like cryptocurrency wallets or online businesses. The goal was to see the full picture, not as a family member, but as the IRS would: as a collection of taxable events waiting to happen.

What surprised me most was how differently assets are treated under tax law. For example, a traditional IRA or 401(k) may seem like a straightforward retirement account during life, but to an heir, it can become a tax burden. When inherited, these accounts are subject to required minimum distributions (RMDs), and each withdrawal is taxed as ordinary income. For a young heir in a high tax bracket, this could mean years of significant tax payments on money they didn’t earn. In contrast, a Roth IRA, if properly funded, can pass tax-free — a crucial difference that many overlook. Similarly, a home may have sentimental value, but from a tax perspective, it’s an illiquid asset that may need to be sold to cover obligations. Investment accounts with low cost bases can trigger large capital gains taxes when sold by heirs, further reducing what they actually receive.

I learned that liquidity, ownership structure, and tax treatment matter more than market value alone. An asset worth $200,000 in a brokerage account is far more useful in covering a tax bill than a $200,000 piece of land that takes months to sell. I began categorizing my assets by these three dimensions: How quickly can it be turned into cash? Who legally owns it, and how will that affect transfer? What tax consequences will the heir face? This exercise revealed gaps in my planning — like having most of my wealth tied up in retirement accounts with no plan for the tax liability they would create. It also showed opportunities, such as converting some traditional IRA funds to Roth over time to reduce future tax exposure. The process was uncomfortable but necessary. You cannot protect what you do not see. And you cannot plan effectively if you view your estate through emotion rather than structure.

Liquidity Crunch: When Heirs Can’t Pay the Bill

Perhaps the most counterintuitive aspect of estate taxes is that they must be paid in cash — and usually within nine months of death. This creates a cruel irony: a family can inherit millions in assets but still face financial crisis if they lack liquid funds. I recall a story from a neighbor whose father left behind a successful small business and a large home. On paper, the estate was worth over $2 million. But nearly all of it was tied up in illiquid assets. The estate tax bill came to nearly $180,000. With no cash reserves set aside, the children had two choices: take out a loan against the business (which strained operations) or sell the home. They chose the latter, even though one sibling had hoped to live in it. The house wasn’t sold because they wanted to — it was sold because they had to. This is what a liquidity crunch looks like: not bankruptcy, but the forced liquidation of legacy assets to meet a government deadline.

The nine-month deadline is not flexible. Interest accrues on unpaid taxes, and the IRS does not accept property in lieu of cash. This means families must either have cash on hand, access to a line of credit, or a prearranged strategy to generate funds quickly. Some turn to life insurance, but as we’ve seen, if the policy is owned by the deceased, the payout may be included in the taxable estate. A better approach is an irrevocable life insurance trust (ILIT), which owns the policy and pays the death benefit directly to the trust, keeping it outside the estate. The trust can then use the funds to cover taxes without forcing asset sales. Another strategy is setting aside a portion of liquid investments — such as a dedicated savings or brokerage account — specifically earmarked for estate costs. This requires discipline, as it means not spending those funds during life, but the payoff is protection during transition.

Strategic gifting during life is another tool to manage liquidity risk. By giving assets to heirs gradually — within the annual gift tax exclusion limit, which is $17,000 per recipient in recent years — individuals can reduce the size of their taxable estate while ensuring heirs receive value earlier. These gifts can be used by recipients to build their own reserves, potentially helping them cover future tax obligations. The key is doing this thoughtfully, not impulsively. Sudden large transfers can trigger gift taxes or affect eligibility for government benefits. But done consistently and within legal limits, gifting becomes a way to transfer wealth with lower risk. The goal is not to give everything away, but to ensure that when the time comes, the family isn’t forced to make painful decisions under pressure. Liquidity isn’t just about money — it’s about preserving choice.

Family Dynamics: How Tax Risks Fuel Conflict

Money has a way of complicating even the closest relationships, especially when it’s tied to loss. I’ve seen families that were once close become estranged after an inheritance, not because of greed, but because of perceived unfairness in how tax burdens were handled. One sibling pays the estate tax from their own savings to keep the family home in the family, but no plan exists for reimbursement. Another inherits a business that generates income but comes with tax liabilities, while a third gets cash that feels easier to manage. Without clear communication, these imbalances breed resentment. The tax bill may be paid, but the emotional cost can last for years.

I’ve come to believe that the most important part of estate planning isn’t the legal documents — it’s the conversations. A few years ago, I initiated what I now call a “family alignment meeting.” I invited my siblings, my parents, and my children to a quiet weekend gathering. We didn’t talk about who would get what. Instead, we discussed values, expectations, and fears. We talked about the possibility of taxes, the importance of fairness, and the role of the executor. We named who would be responsible for managing the process and made sure everyone understood the reasons behind key decisions. It wasn’t easy — emotions ran high at times — but it prevented misunderstandings later. When my father passed, there were no surprises, no accusations, just a shared sense of purpose in carrying out his wishes.

One of the most powerful tools in preventing conflict is transparency. When heirs know in advance about potential tax liabilities, they can plan accordingly. When they understand why one asset is going to a trust and another to a charity, they’re less likely to feel excluded. Documentation helps, but so does dialogue. I’ve learned to include letters of intent alongside legal documents — personal notes explaining the “why” behind decisions. These aren’t legally binding, but they carry emotional weight. They remind heirs that the plan wasn’t made in cold calculation, but in love and foresight. Family harmony isn’t guaranteed by equal distributions, but by mutual understanding. And that understanding must be built long before the will is read.

Advanced Shields: Tools That Actually Work (Without the Hype)

After years of research and consultation with estate attorneys and financial planners, I’ve identified a few strategies that consistently deliver results without overcomplication. The first is the irrevocable life insurance trust (ILIT). Unlike a simple beneficiary designation, an ILIT owns the life insurance policy, meaning the death benefit is not counted as part of the taxable estate. The trust can then use the funds to pay estate taxes, provide income to beneficiaries, or preserve assets without triggering a sale. The trade-off is control: once the trust is established, the grantor typically cannot change the terms or access the funds. But for those willing to make that commitment, the tax savings can be substantial.

Another effective tool is the qualified personal residence trust (QPRT). This allows a homeowner to transfer their primary residence or vacation home into a trust for a set number of years. If the grantor outlives the term, the home passes to heirs at a reduced tax value, often saving significant estate tax. During the trust period, the grantor can continue living in the home, usually paying a nominal rent. It’s not a fit for everyone — it requires careful timing and health considerations — but for homeowners with high-value properties, it can be a powerful way to preserve a legacy.

Annual gifting, when done within exemption limits, is another low-risk strategy. By giving up to $17,000 per year to each heir (or more for educational or medical expenses), individuals can gradually reduce their taxable estate. Over a decade, this can amount to hundreds of thousands of dollars transferred tax-free. The key is consistency and documentation — gifts should be recorded, and funds transferred properly to avoid reclassification by the IRS. These tools are not about getting rich or gaming the system. They are about keeping more of what you’ve built and ensuring it serves the people you care about. There is no one-size-fits-all solution, but there are proven methods that work when applied with intention.

The Long Game: Building a Legacy, Not Just a Payout

What I’ve learned over the years is that estate planning is not a transaction — it’s a process. It’s not something you do once and forget. Laws change. Families grow. Assets shift. A plan that made sense ten years ago may be outdated today. I now review my estate strategy every three years, or after any major life event — a birth, a death, a move, a significant change in net worth. I stay informed about legislative updates, such as changes to exemption levels or tax rates, and I consult professionals who specialize in estate law. This ongoing attention isn’t about fear — it’s about stewardship.

More than anything, I’ve shifted my mindset. I no longer see estate planning as a way to avoid taxes at all costs. Instead, I see it as an act of care. It’s about making sure my children aren’t burdened by decisions I could have made. It’s about preserving the values I’ve lived by — responsibility, fairness, foresight. A legacy isn’t just money. It’s the peace of mind that comes from knowing your family won’t be forced to sell the family home, fight over assets, or face unexpected bills during a time of grief. It’s the quiet confidence that what you’ve built will endure, not because of luck, but because of planning.

The hardest lesson I learned was that ignorance is not innocence. Assuming you’re not wealthy enough to be affected by estate taxes is a risk — and one that can cost your family dearly. But the good news is that it’s never too late to start. Begin with a conversation. List your assets. Talk to a professional. Take one step today. Because the true measure of a legacy isn’t how much you leave behind — it’s how well it’s received.