How I Crushed My Debt with a Smarter Money Game Plan

What if paying off debt didn’t mean living like a hermit? I used to stress over every dollar, but then I shifted my focus—from just cutting costs to allocating assets with purpose. It wasn’t magic, just strategy. By treating debt repayment like a financial reset, not a punishment, I found balance. This is how I turned chaos into control, one smart move at a time—sharing what actually worked. The journey wasn’t about deprivation; it was about redesigning my relationship with money. I stopped seeing every expense as a failure and started viewing my financial decisions as part of a larger, intentional plan. That shift changed everything.

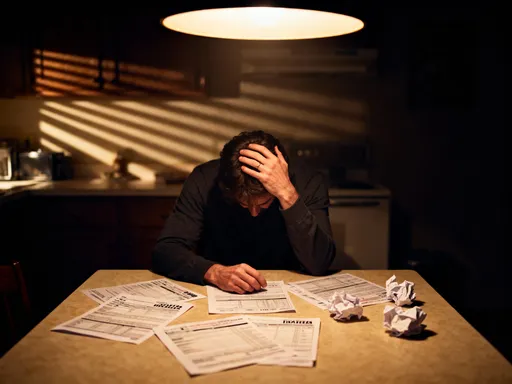

The Breaking Point: When Debt Felt Like a Dead End

There was a time when opening the mailbox filled me with dread. Every credit card statement, every reminder of a missed payment, felt like another nail in the coffin of my financial future. I was juggling four different credit cards, a car loan, and a lingering student debt balance that never seemed to shrink. Each month, I made the minimum payments, believing that consistency alone would get me out. But the numbers told a different story—my balances barely budged, and the interest kept piling up. I had cut back on dining out, canceled subscriptions, and even stopped buying books, yet my net worth was still sinking.

The real wake-up call came when I tried to apply for a small personal loan to cover an unexpected home repair. I was denied—not because of missed payments, but because my debt-to-income ratio was too high. That moment shattered the illusion that I was “managing.” I wasn’t managing; I was treading water while the current pulled me under. I realized that my approach was fundamentally flawed. I had been treating all debt the same, moving money without a plan, and worst of all, I had left my savings idle in a basic checking account earning nothing while my credit card interest climbed to 24%. That imbalance—protecting cash while letting high-interest liabilities grow—was accelerating my financial decline.

What I didn’t understand then was that debt isn’t just a number on a screen; it’s a dynamic force that interacts with every part of your financial ecosystem. By failing to allocate my assets strategically, I was allowing my money to work against me. The turning point wasn’t a sudden windfall or a lifestyle overhaul—it was a decision to stop reacting and start planning. I began to see that financial recovery wasn’t just about earning more or spending less. It was about making smarter decisions with the resources I already had. And that started with a complete reevaluation of how I viewed debt itself.

Reframing Debt: From Burden to Financial Reset

For years, I thought of debt as a moral failure—a sign of poor discipline or lack of willpower. That mindset made repayment feel like punishment, something to endure rather than embrace. But when I began studying personal finance more seriously, I discovered a powerful shift in perspective: debt is not a character flaw; it’s a financial condition that can be managed with strategy. More importantly, I learned to see high-interest debt as a negative asset—one that actively erodes your net worth faster than almost any market downturn. While a stock portfolio might lose 10% in a bad year, a credit card balance at 22% interest diminishes your wealth by that much annually, compounding month after month.

This reframing changed everything. Instead of focusing only on cutting expenses, I began to ask different questions: Where is my money sitting? What is it earning? And more critically, what is it costing me? I realized that traditional budgeting, while helpful, was incomplete without a broader asset strategy. You can cut your grocery bill by $50 a month, but if you’re leaving $5,000 in a zero-interest account while carrying a $3,000 balance at 19%, you’re still losing money. The issue wasn’t just spending; it was allocation.

I started treating my financial recovery like a renovation project. Just as you wouldn’t paint the walls before fixing the foundation, I needed to stabilize my financial base before building wealth. That meant prioritizing high-interest debt not as a chore, but as an investment in myself. Every dollar I paid toward a 20% APR card was effectively earning me a 20% risk-free return—far better than most conservative investments. This perspective made repayment feel productive, even empowering. I wasn’t giving up lattes for nothing; I was redirecting resources to neutralize a financial drain. The goal wasn’t austerity—it was alignment. I wanted my money to work cohesively, not in opposition to my goals.

This mindset shift also helped me avoid the shame that often accompanies debt. I stopped beating myself up for past choices and started focusing on future outcomes. I accepted that mistakes happen, but recovery is always possible with the right approach. By viewing debt repayment as a financial reset—a deliberate step toward stability and freedom—I transformed a source of stress into a catalyst for growth.

The Core Strategy: Asset Allocation for Debt Payoff

Most people think of asset allocation as a concept for investors—how to divide money among stocks, bonds, and cash. But I discovered that the same principles apply to debt repayment. The key insight was this: not all debt is equally dangerous, and not all cash is equally useful. Just as an investor balances risk and return, I needed to balance urgency and flexibility in my debt strategy. That meant categorizing my debts by interest rate, term, and impact, then aligning my available funds accordingly.

I began by listing all my liabilities, from highest to lowest interest rate. The credit card at 23.9% APR became my top priority—this was the financial equivalent of a five-alarm fire. Next was a personal loan at 11%, followed by a car loan at 6.5%, and finally student loans at 4.25%. This hierarchy allowed me to focus my energy where it would have the most impact. But I didn’t stop there. I also assessed my liquid assets. I had $2,000 in a checking account, $1,500 in a savings account earning 0.01%, and another $500 scattered across digital wallets. That money was safe, but it wasn’t working for me.

My strategy became threefold: protect liquidity, neutralize high-cost debt, and minimize opportunity cost. I decided to keep one month’s essential expenses—about $1,800—in an easily accessible account. This wasn’t for debt payments; it was a buffer against emergencies. The rest of my surplus cash would be used strategically. Instead of spreading small payments across all debts, I concentrated on the highest-interest balance first, while still making minimums on the others. This approach mirrored the investment principle of risk-adjusted return: I was allocating my limited resources to the area with the highest payoff.

At the same time, I refused to ignore the importance of liquidity. I didn’t drain my savings to pay off debt faster, because I knew that a single unexpected expense could send me back to square one. Instead, I created a tiered system: a small emergency buffer, a slightly larger surplus fund in a high-yield account, and a clear plan for deploying each. This structure gave me confidence. I wasn’t gambling on perfect circumstances; I was building resilience. The result was a strategy that was aggressive where it needed to be, but also sustainable. I wasn’t just paying off debt—I was rebuilding my financial foundation with intention.

Liquidity vs. Leverage: Keeping Your Options Open

One of the most common financial mistakes I see is the all-or-nothing approach to debt repayment. People empty their savings, pause retirement contributions, or even borrow from 401(k) plans to accelerate payoff. On the surface, this seems logical—every dollar goes to debt, so progress should be faster. But in reality, this strategy often backfires. Without a financial cushion, any surprise—a flat tire, a medical bill, a home repair—forces a return to credit cards, restarting the cycle with even more stress.

I learned this the hard way. Early in my journey, I used $1,200 from my savings to make a large payment on my highest-interest card. Two weeks later, my washing machine broke. With no emergency fund, I had no choice but to put the $450 repair on another credit card. In one month, I erased my progress and added new debt. That experience taught me a crucial lesson: financial strength isn’t just about reducing liabilities; it’s about preserving options. Liquidity is not the enemy of debt payoff—it’s a necessary safeguard.

From that point on, I adopted a more balanced approach. I established a tiered cash strategy with three levels. The first was a bare-minimum buffer—enough to cover one month of essential expenses like rent, utilities, groceries, and transportation. This stayed in a checking account for immediate access. The second tier was a slightly larger emergency fund, growing toward three months’ worth of essentials. This money was kept in a high-yield savings account, earning interest while remaining accessible. The third tier was my surplus fund—extra money beyond what I needed for stability. This was the pool I used to make accelerated debt payments.

This structure allowed me to move aggressively on debt without sacrificing security. When I received a bonus or tax refund, I didn’t automatically send it all to creditors. Instead, I allocated a portion to strengthen my buffer, another to the surplus fund, and the rest to targeted debt reduction. This way, I maintained flexibility. If an emergency arose, I could cover it without derailing my plan. Over time, this balance reduced my anxiety and increased my consistency. I wasn’t white-knuckling my way to freedom; I was building a system that could withstand real life.

Smart Surplus: Where to Park Extra Cash Before Paying Off Debt

Here’s a counterintuitive truth: sometimes, the smartest move isn’t to pay down debt immediately. If you have extra cash, especially if it’s not needed for immediate expenses or emergencies, you have choices. Many people assume that any surplus should go straight to the highest-interest debt. But that’s not always optimal. The key is to consider opportunity cost, liquidity needs, and risk. If you’re holding $2,000 in a zero-interest account while paying 18% on a card, you’re losing value. But if you move that money into a slightly higher-yielding, low-risk vehicle first, you can earn a small return while keeping it available for strategic use.

I discovered this when I started researching high-yield savings accounts. I found options offering 4.5% APY—still far below my 23% credit card rate, but significantly better than 0.01%. I moved my surplus fund into one of these accounts, where it earned interest while remaining accessible. This wasn’t about speculation; it was about efficiency. The goal wasn’t to outearn my debt interest—that was impossible—but to minimize waste. Every dollar that sits idle loses potential. By placing surplus cash in a high-yield account, I was at least making it work, even if modestly.

I also explored short-term certificates of deposit (CDs) for portions of my surplus. A 6-month CD at 4.75% APY wasn’t a game-changer, but it provided a small gain with virtually no risk. I only used this for money I knew I wouldn’t need for at least six months. This approach allowed me to earn a bit more while maintaining discipline. The interest wasn’t enough to offset my debt costs, but it reinforced the habit of intentional allocation. I wasn’t just reacting to debt; I was managing my entire financial picture.

This strategy also gave me psychological flexibility. Seeing my surplus fund grow—even slightly—motivated me to keep going. It reminded me that I wasn’t just paying down debt; I was building financial competence. Over time, as my high-interest balances shrank, I shifted more of this surplus toward investments. But in the early stages, the priority was safety and access. I wanted my money to be ready when I needed it, not locked away or exposed to risk. By treating surplus cash as a strategic resource, not just a debt payment, I created a more resilient and thoughtful path to freedom.

The Payoff Sequence: Balancing Psychology and Math

Debt repayment isn’t just a numbers game—it’s a human one. Two popular methods dominate the conversation: the debt snowball, where you pay off smallest balances first for emotional wins, and the debt avalanche, where you tackle highest-interest debts first for mathematical efficiency. For a long time, I thought I had to choose one. But what I found was that a hybrid approach worked best. I used the avalanche method as my foundation—prioritizing high-interest debt to minimize total interest paid—but I incorporated snowball-style wins to maintain momentum.

Here’s how it worked: my largest interest burden was a credit card at 23.9%. Mathematically, that had to be my focus. But I also had a smaller medical bill of $650 at 0% interest, set to expire in six months. Instead of ignoring it, I decided to pay it off quickly. The psychological boost of eliminating a liability—even a small one—gave me confidence. It proved I could follow through, that progress was possible. That small win made the larger, slower work on the high-interest card feel more manageable.

I applied this principle throughout my journey. When I had a choice between paying an extra $200 toward a $4,000 balance at 18% or a $900 balance at 12%, I considered both the numbers and my motivation. Often, I’d allocate most to the higher-interest debt but leave enough to clear the smaller one within a few months. The moment that smaller debt disappeared, I’d redirect the full payment to the next target. This created a rhythm—a sense of forward motion that kept me engaged.

Consistency, I learned, comes not from willpower but from design. A plan that ignores human psychology is likely to fail, no matter how mathematically sound. By blending logic with emotional reinforcement, I built a system that was both efficient and sustainable. I wasn’t just reducing debt; I was building financial confidence, one clear victory at a time.

Building Wealth After Debt: Turning the Corner

Freedom from high-interest debt isn’t the end of the journey—it’s the beginning of a new phase. Once I paid off my last credit card balance, I didn’t stop. Instead, I repurposed the system I had built. The same discipline, allocation logic, and intentional mindset that helped me eliminate debt became the foundation for wealth building. I took the $400 monthly payment I had been sending to creditors and redirected it toward retirement and investments.

I started by maxing out my IRA contributions, taking advantage of tax-advantaged growth. I also began investing in a diversified portfolio of low-cost index funds, focusing on long-term appreciation. The same principle applied: allocate with purpose. I didn’t jump into speculative stocks or trendy cryptocurrencies. Instead, I treated investing like I had treated debt repayment—methodically, with clear priorities and risk management.

I also revisited my emergency fund, growing it to cover six months of essential expenses. This wasn’t just a safety net; it was a freedom fund. With that cushion in place, I could take appropriate risks in my investments without fear of being derailed by a surprise. I also began setting aside money for specific goals—homeownership, travel, education—using separate high-yield accounts to keep each purpose distinct.

The mindset shift was profound. I no longer saw money as something to be feared or hoarded. I saw it as a tool—a resource to be allocated, grown, and protected. The habits I developed during my debt payoff—tracking expenses, prioritizing high-impact actions, maintaining liquidity—served me even better in the wealth-building phase. I wasn’t starting from scratch; I was building on a solid foundation.

Conclusion

Paying off debt isn’t just about discipline—it’s about design. With the right asset strategy, you don’t just survive the process; you emerge stronger, smarter, and ready to build real financial momentum. I didn’t get here by cutting every luxury or waiting for a miracle. I got here by making thoughtful, strategic decisions about where my money went and why. I treated debt not as a moral failing, but as a financial condition to be managed with intelligence and care. I balanced urgency with sustainability, math with motivation, and risk with resilience. The result wasn’t just a zero balance—it was a new relationship with money. And that, more than any number, is the real victory.