How I Survived a Business Collapse — And What My Investment Strategy Learned

When my company failed overnight, I didn’t just lose income—I lost confidence. But that crisis forced me to rethink everything about money. Instead of chasing quick wins, I focused on resilience. What emerged wasn’t a miracle fix, but a smarter, more balanced investment strategy built for real life. This is how I rebuilt—not just financially, but with clarity, discipline, and a plan that actually works when things go wrong. The journey wasn’t about doubling net worth in a year or uncovering secret markets. It was about learning to protect what I had, earn steadily without gambling, and build a financial foundation that could endure setbacks. That kind of stability doesn’t come from luck. It comes from choices—measured, consistent, and grounded in real-world experience.

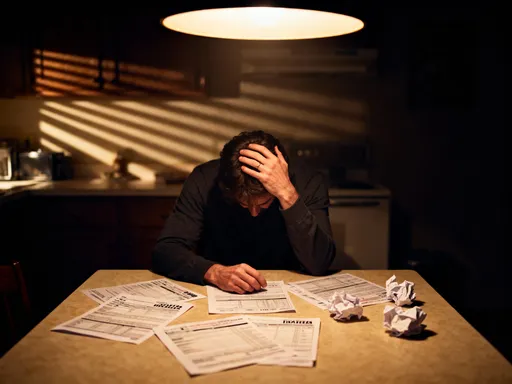

The Breaking Point: When Business Failure Hits Home

The call came on a Tuesday morning. A major client, responsible for nearly 40 percent of our annual revenue, had pulled out. Their decision was abrupt, driven by industry consolidation and shifting consumer behavior—forces we had seen but underestimated. Within weeks, our cash flow dried up. Despite years of steady growth, we had operated with high fixed costs and leveraged credit lines to expand. When income stalled, the debt became unmanageable. By the end of the quarter, the business was insolvent. I closed the doors quietly, paid what I could to creditors, and walked away with nothing but personal savings—savings that now felt terrifyingly small.

The emotional weight was heavier than the financial loss. For over a decade, I had defined myself by my work. Success wasn’t just about money; it was about control, purpose, and independence. Losing the business didn’t just erase income—it shattered my sense of security. Sleep became erratic. Conversations with family carried an undercurrent of anxiety. I started second-guessing every past decision: Why didn’t I diversify revenue sooner? Why did I reinvest so much back into operations without building a personal financial buffer? The answers didn’t matter as much as the realization: I had mistaken business success for personal financial safety. They are not the same.

This moment became a turning point not because it was dramatic, but because it was honest. It stripped away assumptions about wealth and revealed a critical gap—my finances were entirely dependent on a single, fragile source of income. There was no passive income, no diversified portfolio, no emergency plan. I had saved, yes, but those savings were parked in low-yield accounts, untouched and unmanaged. I had treated investing as something distant, something to start “when I had more time” or “after the next big contract.” Now, time had run out, and I was left exposed. The collapse didn’t just cost me a business; it cost me peace of mind. But from that loss came a quiet determination: I would never again confuse income with financial security.

From Loss to Learning: Why Traditional Investing Failed Me

In the months that followed, I revisited the financial advice I had long accepted as truth. Diversify your portfolio. Invest early and often. Stay the course through market cycles. These principles sounded wise in theory, but in practice, they offered little comfort when both my business and my stock investments were falling at the same time. My portfolio, mostly in broad-market index funds and a few growth stocks, dropped nearly 30 percent during the same period my business collapsed. There was no income to replenish those losses, no sidelines to retreat to. I was forced to sell some holdings at a loss to cover living expenses—locking in damage just when I could least afford it.

That experience exposed a flaw in conventional wisdom: most mainstream investing advice assumes a stable income stream. It presumes you can keep contributing to your accounts, ride out downturns, and wait decades for recovery. But what happens when your income vanishes? When you need cash now, not in 20 years? The traditional model doesn’t account for that vulnerability. It treats investing as a long-term game played in isolation from life’s disruptions. In reality, financial health depends on coordination between income, savings, and investments—and when one pillar fails, the others often follow.

I also began to recognize how psychological bias had shaped my decisions. Before the collapse, I had been overconfident. Success bred complacency. I ignored warning signs in the market because I believed my business was immune. When the downturn hit, fear took over. I froze, then reacted impulsively—selling low, hesitating to rebuy, missing early recovery signals. The absence of a clear strategy left me at the mercy of emotion. I realized then that investing isn’t just about picking assets; it’s about managing behavior. Without rules, discipline, and safeguards, even a well-diversified portfolio can fail when stress and uncertainty take control.

The lesson wasn’t that traditional investing is wrong—it’s that it’s incomplete. For someone with a stable job and predictable income, passive indexing can work well. But for entrepreneurs, self-employed individuals, or anyone with volatile earnings, a different approach is needed. One that prioritizes liquidity, reduces reliance on perfect timing, and builds in protection before crisis strikes. I didn’t need more aggressive growth. I needed resilience—the ability to withstand loss without derailing long-term goals.

Building a Crisis-Proof Strategy: The Core Principles

Out of that painful period, a new framework emerged. It wasn’t born from complex algorithms or exotic financial products, but from practical necessity. I built my strategy around three core principles: capital preservation, income redundancy, and adaptive allocation. Each one addressed a specific vulnerability exposed by the collapse. Together, they formed a system designed not for maximum returns, but for survival and steady progress—even in difficult times.

Capital preservation became the foundation. This means protecting the principal value of investments as the first priority, not chasing high returns at the risk of large losses. It’s the financial equivalent of wearing a seatbelt: you don’t expect a crash, but you prepare for one. In practice, this meant shifting a significant portion of my portfolio into assets with limited downside—short-duration bonds, high-quality fixed-income securities, and cash equivalents. These don’t generate spectacular gains, but they hold value when markets fall. They also provide a source of funds during emergencies, reducing the need to sell stocks at a loss.

Income redundancy was the second pillar. Instead of relying on one dominant source of earnings, I began building multiple streams of income—some active, some passive. This included rental income from a small real estate investment, dividends from carefully selected stocks and funds, and income from part-time consulting work. The goal wasn’t to replace my former business income overnight, but to create a buffer. If one stream dried up, others could help cover expenses. This diversification of income reduced pressure on my investment portfolio and gave me breathing room during transitions.

The third principle, adaptive allocation, replaced rigid, set-and-forget investing with a dynamic approach. Rather than sticking to a fixed asset mix regardless of market conditions, I began adjusting my portfolio based on risk levels, economic signals, and personal circumstances. For example, during periods of high market volatility, I increased my cash and bond holdings. When valuations appeared favorable, I gradually added to equity positions. This isn’t market timing in the speculative sense—it’s risk-aware allocation. It acknowledges that markets change, and so should our strategies. The key is to make adjustments systematically, not emotionally.

Putting It Into Practice: Tactical Shifts That Made a Difference

With these principles in place, I began making concrete changes to my portfolio. The first step was reducing exposure to high-volatility equities—especially speculative growth stocks that had once seemed promising but lacked consistent earnings. I sold a portion of these holdings not because I expected a crash, but because their risk profile no longer matched my needs. The proceeds were reinvested into hybrid assets that offered both income and downside protection. One example was a diversified fund focused on dividend-paying companies with strong balance sheets and a history of maintaining payouts through economic cycles. These companies aren’t the fastest growers, but they tend to be more stable and provide regular cash flow.

I also allocated a portion of my portfolio to tangible assets, including a small investment in a residential property that I rent out. Real estate doesn’t move in lockstep with the stock market, which helps reduce overall portfolio correlation. The rental income covers the mortgage and generates a modest surplus, which I reinvest. While real estate requires management and carries its own risks, it provides a sense of control and a physical asset that holds intrinsic value. Additionally, I added short-duration investment-grade bonds, which offer higher yields than savings accounts with relatively low interest rate risk. Because they mature quickly, I can reinvest the principal as rates change, avoiding long-term exposure to rising rates.

Another critical change was implementing systematic rebalancing. Instead of reacting to market swings, I set a schedule—quarterly reviews—to assess my asset allocation. If equities had grown to represent more than 60 percent of my portfolio due to strong performance, I would sell a portion and redirect the funds into bonds or cash. If bonds had outperformed and equities dropped, I would gradually add to stock positions. This discipline ensures I’m consistently buying low and selling high over time, without having to predict market movements. It removes emotion from the process and enforces balance.

Timing and patience proved more valuable than instinct. I didn’t try to jump back into the market at the exact bottom, nor did I panic when prices dipped again. Instead, I used dollar-cost averaging—investing fixed amounts at regular intervals—into broad-market index funds. This approach smoothed out entry points and reduced the risk of making a single bad decision. The results weren’t dramatic, but they were steady. Over two years, my portfolio recovered its value and began growing again—this time with less stress and more confidence in the underlying structure.

Risk Control as a Daily Habit, Not an Afterthought

One of the most important shifts was treating risk management as a daily practice, not a one-time setup. I developed personal rules to prevent emotional decision-making. For example, I defined clear exit criteria for each investment: if a stock dropped 15 percent due to fundamentals weakening, not just market noise, I would reassess. I also set position limits—no single holding could exceed 5 percent of my portfolio—so no one loss could severely damage my overall finances.

I created a pre-trade checklist that I review before making any significant investment move. It includes questions like: Does this align with my long-term goals? Have I assessed the downside risk? Am I reacting to fear or greed? Is this decision based on data or emotion? Simply pausing to answer these questions has prevented impulsive actions during turbulent times. I also began using stop-loss orders on certain holdings—not as a way to avoid all losses, but as a tool to enforce discipline and prevent small losses from becoming large ones.

Scenario planning became part of my routine. I regularly ask myself: What if the market drops 20 percent? What if I lose my consulting income? What if interest rates rise sharply? For each scenario, I outline potential responses in advance. This doesn’t mean I can predict the future, but it means I’m not starting from scratch when trouble hits. I’ve already thought through my options, so I can act calmly instead of reacting in panic. These habits don’t eliminate risk, but they make it manageable. They turn uncertainty from a source of fear into a factor I can plan for.

Earning While Protecting: The Search for Resilient Returns

Growth still matters, but on safer terms. My goal is no longer to outperform the market every year, but to achieve consistent, sustainable returns with limited drawdowns. I focus on income-generating assets that don’t require high volatility. Dividend-focused exchange-traded funds (ETFs) have become a core holding. These funds pool shares of companies with a history of paying and increasing dividends, offering diversification and regular cash flow. I reinvest the dividends during downturns to buy more shares at lower prices, accelerating recovery when markets rebound.

I also explored structured notes with principal protection features—financial instruments issued by banks that offer upside potential linked to market performance while limiting downside risk. While these are not suitable for everyone and require careful evaluation, they provided a way to participate in market gains without full exposure to losses. I allocated only a small portion of my portfolio to such products, ensuring they didn’t compromise overall liquidity.

Real estate remains a part of my strategy, but selectively. I avoided over-leveraging and focused on properties in stable rental markets with reliable tenant demand. The income isn’t huge, but it’s predictable and helps offset inflation. I also looked into peer-to-peer lending platforms that offer fixed-income returns by funding small loans to individuals or businesses. These carry credit risk, so I diversified across many small loans and used only a fraction of my portfolio for this purpose.

The key in every decision is balance. I evaluate each opportunity not just by its potential return, but by its risk of loss, liquidity, and alignment with my broader financial plan. Yield is important, but sustainability matters more. A 7 percent return means little if it comes with a 40 percent chance of losing half the principal. I’d rather earn 4 percent with confidence than gamble on 8 percent with anxiety.

Lessons Beyond the Balance Sheet: Mindset, Time, and Second Chances

The most profound changes weren’t in my portfolio—they were in my mindset. Business failure forced me to confront my relationship with money, risk, and self-worth. I used to measure success by growth, scale, and income. Now, I measure it by stability, freedom, and peace of mind. The real return on my new investment strategy isn’t just financial—it’s emotional. I sleep better. I make decisions with clarity, not fear. I have the freedom to say no to opportunities that don’t align with my values or risk tolerance.

Time, once something I felt I was racing against, has become an ally. I no longer expect quick fixes or overnight success. I accept that building lasting financial security is a gradual process, like tending a garden. Some seasons yield more than others, but consistent care produces results over time. I’ve learned to appreciate small wins: a dividend payment that covers groceries, a bond maturing at the right moment, a market dip that allows me to buy quality assets at a discount.

Most importantly, I’ve learned that failure isn’t final. It can be a teacher, a reset, a second chance. The collapse of my business was devastating, but it led me to a more thoughtful, disciplined, and resilient approach to money. I no longer chase returns. I build foundations. I don’t try to predict the future. I prepare for it. And in doing so, I’ve gained something more valuable than wealth: the confidence that no matter what happens, I have a plan that can carry me through.