How I Survived a Business Crash and Still Protected My Returns

Losing a business is gut-wrenching — I’ve been there. When mine collapsed, I thought all my money was gone for good. But through smart moves and tough lessons, I managed to shield part of my returns when everything else fell apart. In this article, I’ll walk you through the real strategies that helped me survive financially. No hype, no false promises — just practical steps I tested when the pressure was highest. This isn’t a story of instant recovery or miraculous windfalls. It’s about making hard choices, thinking ahead, and protecting what you’ve built even when the ground gives way beneath you. If you’ve ever feared losing it all, this is for you.

The Moment Everything Crashed

It started with a single phone call. A major client was pulling out — not just reducing orders, but canceling their contract entirely. That account represented nearly 40 percent of our monthly revenue. I remember sitting at my desk, staring at the numbers on the screen, trying to calculate how long we could last without that income. The answer was less than three months. Within weeks, suppliers began demanding faster payments. Overdue invoices piled up. Employees asked quietly about their bonuses. The energy in the office changed — tense, uncertain, fragile.

By the third month, we were no longer breaking even. We were burning through savings just to keep the lights on. I had poured nearly all my personal capital into the company over five years, believing in its long-term potential. Now, that belief felt like a mistake. The emotional toll was worse than the financial one. There’s a unique kind of shame that comes with business failure — a feeling that you’ve let down your team, your family, and yourself. I stopped answering calls from friends who had invested small amounts. I avoided networking events. The weight of responsibility was crushing.

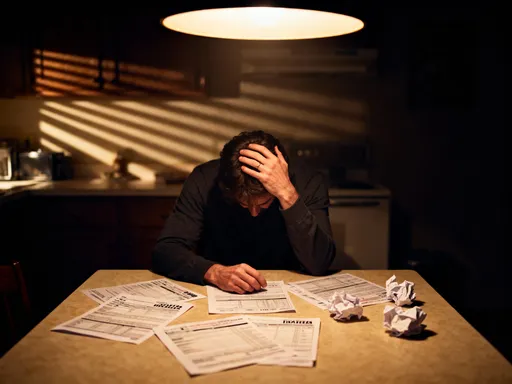

Then came the final blow: a lawsuit from a partner over a disputed agreement. Legal fees spiked. Cash reserves vanished. I made the decision to close operations. That night, I sat at my kitchen table, surrounded by spreadsheets and bank statements, trying to understand what was left. The business was insolvent. Debts exceeded assets. I believed I had lost everything — including any chance of recovering personal returns. But in the days that followed, I realized something crucial: even in collapse, there are still decisions to make. And those decisions can determine how much — or how little — you ultimately lose.

Why “Return Guarantee” Doesn’t Mean What You Think

Before my business failed, I used to believe that certain investments or business structures offered a kind of safety net — something close to a return guarantee. I assumed that if I followed the rules, worked hard, and reinvested profits, I would eventually get my money back, no matter what. But that’s not how finance works. There is no such thing as a true return guarantee in the real world of business and investment. Every venture carries risk, and the idea that you can fully protect your capital is a dangerous illusion.

What I learned the hard way is that “return guarantee” should be redefined — not as a promise of profit, but as a disciplined approach to capital preservation. It’s about stacking the odds in your favor through structure, timing, and foresight. For example, in private equity and venture deals, investors often negotiate liquidation preferences, which give them priority access to remaining assets if a company fails. These aren’t guarantees, but they increase the likelihood of recovering at least part of the investment. Similarly, secured loans backed by physical assets provide more protection than unsecured ones because the lender can seize and sell the collateral.

Another key concept is downside protection. This doesn’t mean avoiding loss altogether — that’s impossible — but minimizing it when things go wrong. Instruments like put options in investing, stop-loss orders, or even conservative leverage ratios are tools designed to limit exposure. In my case, I had unknowingly built some of this protection into earlier contracts by insisting on partial upfront payments and performance-based milestones. Those clauses didn’t save the business, but they did allow me to recover a small portion of receivables before operations ceased.

The takeaway is this: financial security doesn’t come from false promises of guaranteed returns. It comes from understanding that risk is inevitable and designing your financial strategy around that truth. Expecting complete protection sets you up for disappointment. But planning for partial recovery — and building mechanisms to support it — can make the difference between total loss and survival.

Building Your Safety Net Before Disaster Hits

Looking back, the most painful realization isn’t that I lost money — it’s that I could have done more to protect it. The foundation for financial resilience isn’t laid during a crisis. It’s built long before, in the quiet moments when everything seems stable. That’s when the smartest moves are made — not out of panic, but out of planning. The strategies I now rely on weren’t invented in desperation; they were adopted too late, after I’d already seen the cost of neglecting them.

One of the most effective tools I wish I’d used earlier is the clawback provision. This is a contractual clause that allows investors or owners to reclaim funds under certain conditions — for example, if financial statements are later found to be inaccurate or if key performance targets aren’t met. In industries where revenue recognition is complex, such as consulting or software services, these clauses can prevent overpayment and preserve capital. I had avoided including them in early partnership agreements, thinking they would seem distrustful. Now I see them as standard risk management — not a sign of suspicion, but of prudence.

Another critical step is using escrow arrangements for large transactions. When selling products or services with long delivery cycles, placing a portion of the payment in escrow ensures that funds are available even if the buyer defaults. In my final year, I had several clients who delayed payments for months. Had I structured those deals with third-party escrow, I might have recovered tens of thousands in disputed invoices. Escrow isn’t just for real estate — it’s a powerful tool in any business dealing with delayed fulfillment or high-value contracts.

Asset structure also matters. I made the mistake of purchasing expensive equipment outright, thinking it would be a long-term investment. When the business failed, selling those assets yielded only a fraction of their original cost. Had I leased instead, I would have avoided ownership risk and preserved cash. Similarly, I overlooked the resale value of certain assets — like proprietary software templates or customer databases — that could have been licensed or sold to competitors. The lesson is clear: prioritize assets that retain value and can be liquidated efficiently. Protection begins not when the storm hits, but when the sky is still clear.

When the Floor Drops — What to Do in the First 72 Hours

When a business begins to fail, the first 72 hours are critical. Emotions run high. Decisions feel overwhelming. But this is exactly when clarity matters most. Panic leads to poor choices — like selling assets too quickly, ignoring creditor communications, or shutting down systems without preserving records. I made several of these mistakes, and each one cost me money and future options. What I’ve learned is that having a crisis response plan — even a simple one — can dramatically improve your chances of financial recovery.

The first step is to freeze all non-essential spending. That means pausing marketing budgets, travel, subscriptions, and discretionary purchases. It also means reviewing every recurring expense — from software licenses to insurance policies — and canceling what isn’t immediately necessary. In my case, I kept paying for cloud storage, accounting software, and a virtual assistant long after operations had stopped. These small monthly charges added up and drained what little cash remained. A spending freeze isn’t about cutting corners — it’s about conserving resources for higher-priority actions.

The second priority is communication. Many people avoid talking to creditors when they’re in trouble, hoping the problem will go away. It won’t. Proactively contacting lenders, suppliers, and service providers shows responsibility and can open doors to negotiation. I delayed this step for nearly two weeks, afraid of confrontation. When I finally reached out, I discovered that several creditors were willing to restructure payments or accept partial settlements. Some even offered temporary forbearance. Had I acted sooner, I might have preserved more goodwill and flexibility.

The third essential action is securing records. This includes financial statements, tax filings, customer contracts, email archives, and digital backups. When a business closes, these documents may be needed for audits, legal disputes, or tax purposes. I lost access to an old server because I hadn’t updated login credentials, and that complicated my tax filing for the year. Today, I maintain a secure, offline backup of all critical files — a habit I now treat as non-negotiable. The first 72 hours aren’t about fixing the business. They’re about protecting your financial position as the situation unfolds.

Turning Assets into Cash Without Losing Everything

Once the immediate crisis is managed, the next challenge is converting remaining assets into usable cash. This isn’t about maximizing value — in a downturn, that’s rarely possible. It’s about avoiding fire-sale prices and extracting as much liquidity as you can without surrendering everything. I learned this the hard way when I tried to sell office furniture, computers, and inventory in a rush. Buyers knew I was desperate, and they offered prices far below market value. I accepted most of them, just to clear space and move on. In hindsight, I could have done much better.

The key is to balance speed and value. Some assets need to be sold quickly — especially those that depreciate fast or incur storage costs. Others can wait for better offers. For example, I had custom-built display units that were expensive to store. Selling them through an online auction platform brought in modest returns, but it was better than letting them gather dust. On the other hand, I had a small portfolio of digital content — training videos and templates — that I eventually licensed to another company. That deal took months to finalize, but it generated steady royalty income for over a year.

Another option is using brokers or intermediaries for high-value items. While they take a commission, their networks and negotiation skills often result in higher sale prices than private listings. I sold a company vehicle through a local dealership rather than a classified ad — they handled the paperwork, marketing, and buyer screening, and the final price was 25 percent higher than my initial asking price. For intellectual property, such as trademarks or software, consulting a specialist can help identify potential buyers in adjacent industries.

Online marketplaces like eBay, Craigslist, or industry-specific platforms can also be effective, especially for niche equipment. The key is presentation: clear photos, accurate descriptions, and realistic pricing attract serious buyers. I also discovered that selling in bundles — for example, grouping office chairs, desks, and filing cabinets — made the offer more appealing and reduced negotiation time. The goal isn’t to recover everything, but to salvage what you can, piece by piece, with patience and strategy.

Learning the Hard Way — Mistakes I Wish I’d Avoided

No one plans to fail, but everyone makes choices that increase the risk of it happening. In my case, some of the most damaging mistakes weren’t financial — they were behavioral. I ignored early warning signs because I was too focused on growth. I delayed tough conversations with partners because I wanted to maintain harmony. I overestimated customer loyalty, assuming that long-term relationships would protect us during hard times. They didn’t. Each of these decisions seemed minor at the time, but together, they eroded our resilience.

One of the biggest errors was failing to diversify revenue streams. We relied heavily on a few large clients, and when one left, the impact was catastrophic. I had turned down opportunities to expand into new markets or develop complementary services because I thought specialization was the path to success. Now I see that over-reliance on any single source of income is a vulnerability. Diversification isn’t just for investors — it’s a survival strategy for businesses too.

Another mistake was poor cash flow management. I focused on revenue and profit margins but didn’t track cash flow with the same rigor. We had periods of high sales but still struggled to pay bills because payments were delayed. I didn’t implement strict invoicing policies or follow up consistently on overdue accounts. By the time I realized how thin our reserves were, it was too late to adjust. Today, I review cash flow weekly and maintain a minimum reserve equivalent to three months of operating expenses.

I also underestimated the importance of legal and financial documentation. Contracts were often verbal or loosely written. Equity agreements weren’t formalized. When disputes arose, I had little recourse. I’ve since learned that clarity in agreements isn’t about distrust — it’s about protection. Every business relationship, no matter how friendly, should be documented with clear terms, exit clauses, and dispute resolution mechanisms. These aren’t signs of pessimism. They’re tools of professionalism and foresight.

Coming Back Stronger — Rebuilding with Smarter Rules

Recovery doesn’t happen overnight. It’s a slow process of rebuilding confidence, credit, and capital. After my business closed, I took a year to reflect, study, and plan. I didn’t rush into another venture. Instead, I focused on understanding what went wrong and how to do better. That time wasn’t wasted — it was investment in future resilience. Today, I run a smaller but more sustainable operation, built on lessons learned the hard way.

One of the most important changes is my approach to risk. I no longer chase high returns without considering the downside. I prioritize stability over speed. My new business operates with conservative leverage, meaning I avoid excessive debt and maintain strong liquidity. I’ve also diversified income streams — consulting, digital products, and partnerships — so that no single client can jeopardize the entire operation. This doesn’t mean I’ve become risk-averse. It means I manage risk deliberately, with systems in place to absorb shocks.

I’ve also adopted stricter financial controls. I use automated accounting software to track every transaction in real time. I conduct quarterly financial reviews with an independent advisor. I’ve set personal and business budget caps that I don’t exceed, even during good months. These habits create discipline and prevent overextension. I’ve learned that financial health isn’t measured by peak earnings, but by consistency and sustainability.

Most importantly, I’ve shifted my mindset. Failure used to feel like an ending. Now I see it as a pivot — a painful but necessary step in the journey. Protecting returns isn’t about avoiding loss. It’s about minimizing damage, learning from mistakes, and staying ready for the next opportunity. The goal isn’t perfection. It’s resilience. And that, more than any single success, is what defines long-term financial survival.