What No One Tells You About Early Education Costs

We all want the best start for our kids, but early education expenses can sneak up like an uninvited guest. I learned this the hard way—what seemed like small monthly fees quickly snowballed. Daycare, preschool, learning materials, extracurriculars—they add up faster than you think. Worse, most families don’t see the financial risks until they’re already in too deep. This is a reality check, not a sugar-coated guide. While early education is valuable, the costs are often underestimated, and the long-term impact on household finances can be profound. Understanding these expenses isn’t about cutting corners—it’s about making informed choices that support both your child’s development and your family’s financial health.

The Hidden Price Tag of “Just Preschool”

When parents hear the word "preschool," many assume it’s a modest expense—something manageable on a middle-income budget. But the reality is far more complex. Tuition is just the beginning. Enrollment deposits, non-refundable application fees, and annual registration charges often appear before the first day of class. These upfront costs can range from a few hundred to over a thousand dollars, depending on the program, and are rarely included in advertised pricing. Once enrollment is secured, recurring fees follow: weekly or monthly tuition, transportation, meal plans, and activity charges for field trips or seasonal events. These may seem small in isolation, but together, they form a steady outflow that strains even well-planned budgets.

Then there are the indirect costs—classroom supplies, labeled clothing, special shoes for gym days, holiday gifts for teachers, and donations for classroom materials or school events. Some schools expect families to contribute art supplies, tissues, or cleaning wipes on a monthly basis. Others host fundraising campaigns that carry subtle social pressure to participate. While none of these items are individually large, their cumulative effect over a two- or three-year preschool period can total thousands of dollars. A 2022 report from the U.S. Department of Education noted that families with children in private early education programs spent an average of $11,000 annually when all associated costs were included—not just tuition. For many households, that’s equivalent to a second mortgage payment or a major household expense.

What makes this financial burden harder to track is its fragmented nature. Unlike a single car payment or rent agreement, early education costs come in many forms and at irregular intervals. A birthday donation here, a supply list there—these expenses blend into daily life until they’ve taken a significant share of disposable income. The psychological effect is subtle: because no single charge feels excessive, families rarely pause to assess the total. Yet over time, this steady drain can delay other financial goals, from saving for a home to building an emergency fund. Recognizing the full scope of these costs is the first step toward financial clarity.

Why Early Spending Feels “Safe” (But Isn’t)

One of the most dangerous aspects of early education spending is how emotionally justified it feels. Parents are told—by experts, by society, by other parents—that early childhood is a critical window for development. The message is clear: invest now, or risk falling behind. This creates a powerful narrative that spending on preschool is not discretionary but essential. As a result, families often treat these expenses differently than other large purchases. There’s no comparison shopping for a car, no negotiation of terms, no second thoughts about affordability. The decision is made quickly, driven by love and concern rather than financial analysis.

This emotional framing makes early education spending feel safe, even when it isn’t. Unlike buying a house or planning for college, where families typically assess affordability, interest rates, and long-term impact, preschool decisions are often made in a vacuum. There’s little discussion about return on investment, long-term financial strain, or alternative options. The assumption is that more spending equals better outcomes, but research does not consistently support this. A longitudinal study by the National Institute for Early Education Research found that while high-quality preschool has benefits, the difference between mid-tier and premium programs is often marginal in terms of long-term academic performance. Yet families continue to pay premium prices, believing they are securing a significant advantage.

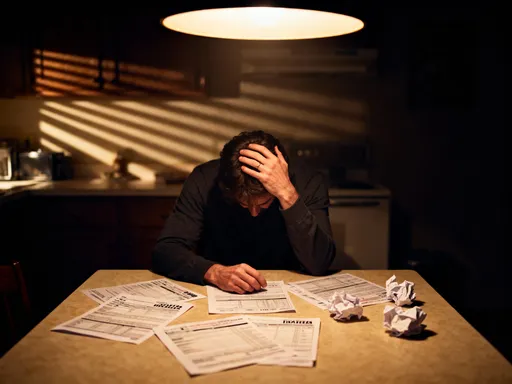

The danger lies in the invisibility of compounding costs. Because payments are spread over months or years, they don’t trigger the same financial alarm as a one-time expense. A $300 monthly fee feels manageable—until it’s joined by another $50 for enrichment classes, $25 for snacks, and $100 for a spring festival. These add-ons accumulate quietly, and by the time families realize how much they’re spending, they’re already committed. The result is a financial anchor: a fixed expense that limits flexibility and reduces the ability to respond to unexpected challenges. Breaking this cycle requires shifting from emotional decision-making to intentional planning.

The Risk of Overcommitting Before Stability

Many families make early education decisions at a time of maximum financial uncertainty. The years surrounding a child’s birth often include income disruptions—maternity or paternity leave, reduced work hours, or career shifts. Yet this is also when parents feel the most pressure to provide the “best” start. The combination of emotional urgency and financial vulnerability creates a perfect storm for overcommitment. Signing a contract for a premium preschool program may feel like a responsible choice, but doing so without a stable income or emergency savings can lead to serious consequences.

Consider a real-life scenario: a dual-income family enrolls their child in a high-end daycare program at $1,200 per month. Both parents are employed, and the budget seems to allow it. But six months in, one parent loses their job due to company restructuring. Suddenly, that monthly fee represents nearly 20% of the household’s remaining income. The family faces a painful choice: drain savings, go into debt, or switch to a lower-cost option that may be less convenient or farther from home. In many cases, families choose the first two options, compromising long-term stability to maintain short-term consistency. Credit card debt, personal loans, or withdrawals from retirement accounts become the hidden cost of early education.

The problem isn’t the desire to provide quality care—it’s the lack of alignment between spending and financial capacity. Too often, families prioritize early education over building a safety net. They commit to fixed expenses before establishing a three- to six-month emergency fund or securing adequate insurance. This imbalance leaves them exposed. A medical emergency, car repair, or home issue can quickly turn a manageable budget into a crisis. The lesson isn’t to avoid quality programs, but to time commitments wisely. Delaying enrollment by a few months to build savings, choosing a part-time schedule initially, or starting with a community-based option can reduce risk without sacrificing care.

Opportunity Cost: What You’re Really Giving Up

Every financial decision involves trade-offs, and early education is no exception. When a family spends $12,000 a year on preschool, that money is no longer available for other goals. The immediate benefit—a structured learning environment for a young child—is visible and emotionally rewarding. The hidden cost—the lost opportunity to save or invest—is invisible but equally real. This is the concept of opportunity cost: what you give up when you choose one path over another.

Consider this: $12,000 invested annually from age 0 to 5, with a modest 6% annual return, would grow to over $85,000 by the child’s 18th birthday. That sum could cover a significant portion of college tuition, a down payment on a first home, or a launchpad for a small business. Instead, when that money goes toward preschool, the long-term financial benefit is uncertain. While early education has developmental value, it does not guarantee higher income, better grades, or greater success. The return is social and cognitive, not financial. For many families, this trade-off is worth it. But the key is making it consciously, not by default.

Other trade-offs include delayed homeownership, reduced retirement savings, and limited ability to handle emergencies. A family that spends heavily on early education may postpone buying a home because they haven’t saved enough for a down payment. Another may reduce 401(k) contributions, missing out on employer matches and compound growth. These effects accumulate over time, reshaping the family’s financial trajectory in ways that aren’t immediately obvious. A 2021 Federal Reserve report found that households with children were more likely to report financial stress, with early care costs cited as a major factor. The message is clear: spending on early education isn’t free. It comes at the expense of other priorities, and those sacrifices deserve careful consideration.

Spotting Red Flags Before You Sign

Not all early education programs offer the same value, yet many charge similar prices. This discrepancy creates financial risk for families who assume higher cost equals higher quality. To protect their budgets, parents must learn to identify red flags that signal poor value or hidden pressure. One major warning sign is high-pressure sales tactics. Some programs use limited enrollment, fear-based messaging, or time-sensitive discounts to rush families into decisions. Phrases like "spots fill fast" or "enroll now to secure your child’s future" are designed to bypass rational thinking. Reputable programs provide information, answer questions, and allow time for reflection—they don’t pressure.

Another red flag is a lack of transparency. If a school’s website doesn’t list tuition, or if staff are vague about what’s included in the fee, that’s a concern. Hidden costs—like technology fees, facility upgrades, or mandatory donations—can add 20% or more to the base price. A clear, written contract that details all charges is essential. Similarly, non-refundable deposits or cancellation fees that exceed one month’s tuition should raise caution. These terms lock families in and reduce flexibility, making it harder to respond to changes in income or family needs.

Curriculum vagueness is another warning sign. A program that emphasizes branding, luxury facilities, or celebrity endorsements over concrete learning goals may be prioritizing marketing over education. Ask specific questions: What teaching methods are used? How are children assessed? What qualifications do the teachers have? A high-quality program can provide clear, evidence-based answers. If the response is filled with buzzwords but lacks substance, it may not be worth the premium price. Families who take the time to compare options, ask questions, and read reviews are better positioned to make value-aligned choices.

Building a Smarter, Safer Approach

Financially resilient families don’t avoid early education—they plan for it. The key is to treat it as a strategic decision, not an emotional reflex. Start by setting a cost limit based on your household income. A common guideline is to spend no more than 10% of gross income on childcare, though this varies by location and family size. Once a budget is set, stick to it. This doesn’t mean choosing the cheapest option, but rather finding the best value within your range. Quality can exist at different price points, especially in community-based or cooperative programs.

Timing also matters. If possible, delay full-time enrollment until income is stable or savings are in place. Many programs offer part-time or drop-in options that provide structure without the full financial commitment. Others allow trial periods, giving families a chance to assess fit before signing long-term contracts. Staggering enrollment—starting with two days a week and increasing gradually—can ease the financial transition. Some families coordinate with trusted relatives or form childcare co-ops with other parents, sharing costs and responsibilities.

Flexibility is another cornerstone of a smarter approach. Choose programs with month-to-month options or short notice periods for cancellation. Avoid long-term contracts unless they offer significant savings and you’re confident in your financial outlook. Look for employers who offer dependent care flexible spending accounts (FSAs), which allow pre-tax dollars to be used for qualified childcare expenses. In the U.S., this can save families hundreds or even thousands per year. Additionally, some states offer subsidies or tax credits for low- and middle-income families, reducing the net cost of care. Taking advantage of these tools doesn’t mean compromising on quality—it means being resourceful.

Long-Term Gains Start With Short-Term Clarity

The best start for a child isn’t just about academics or enrichment—it’s about stability. A home free from financial stress, parents who aren’t overwhelmed by debt, and a family with a plan for the future create a foundation that lasts far longer than any preschool curriculum. Early education matters, but it should enhance, not endanger, a family’s financial health. The goal isn’t to eliminate spending, but to make it intentional, balanced, and sustainable.

This requires a shift in mindset. Instead of asking, "What’s the best program I can find?" families should ask, "What’s the best program I can afford without compromising other goals?" It’s a subtle difference, but a powerful one. It moves the focus from comparison and competition to clarity and control. It allows parents to make choices based on values, not fear. And it opens the door to creative solutions that deliver quality without strain.

True financial wellness isn’t about perfection—it’s about awareness. It’s understanding that every dollar has a purpose and that trade-offs are inevitable. By recognizing the real cost of early education, spotting financial risks early, and planning with intention, families can avoid the trap of silent strain. They can give their children a strong start while protecting their long-term security. Because in the end, the most valuable gift a parent can give isn’t the most expensive preschool—it’s peace of mind, stability, and a future built on solid ground.